Why is Cashback Important for Buyers?

How Cashback Rewards Help Consumers Save More in a World of Rising Prices.

Prices are rising. Groceries cost more. Fuel is expensive. Rent keeps climbing. And yet, most people are still shopping the same way they always have — without earning a single dollar back on what they spend.

That’s where cashback comes in. It’s one of the simplest, most powerful tools a buyer has today. And unlike coupons or flash sales, cashback works quietly in the background — rewarding you every time you make a purchase, without asking you to change a thing about how you live.

In this article, we’ll break down exactly why cashback is important for buyers, how it helps in a time of rising costs, and how you can start earning cashback on everyday purchases — including through gift card platforms that have made rewarding buyers their core focus.

What Exactly is Cashback?

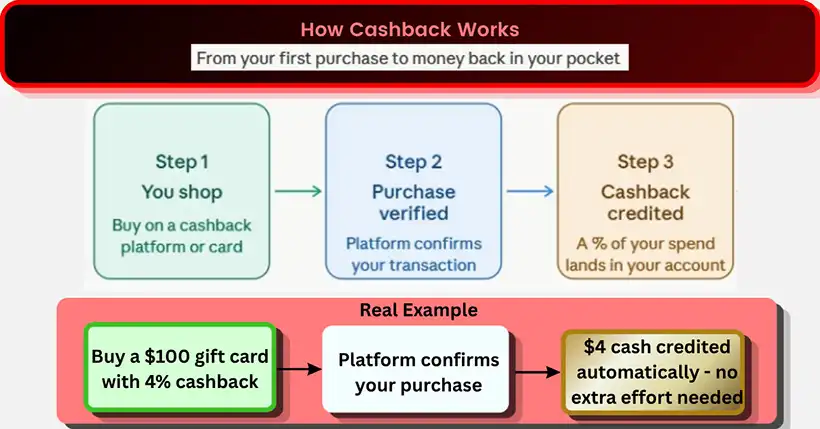

Cashback is a financial incentive where a buyer receives a percentage of the money they spent on a purchase. It can come in the form of real money credited to your account, points redeemable for future purchases, or credits applied to your next transaction.

The concept is straightforward: you spend $1,00, and if the cashback rate is 5%, you get $5 back. You didn’t do anything differently. You didn’t hunt for a discount code. You just shopped — and the system rewarded you for it.

|

Think of cashback as your money working backwards. You pay first, and a portion finds its way back to you — automatically, reliably, without effort. |

|---|

Cashback programmes exist across credit cards, e-commerce platforms, banking apps, and increasingly, gift card platforms. Each has its own rules, rates, and redemption methods — but the core idea is always the same: reward the buyer for spending.

Why Cashback Matters More Than Ever Right Now

A few years ago, cashback was a nice-to-have. Today, with inflation squeezing household budgets across the country, it has become a genuine financial tool that consumers cannot afford to ignore.

Here’s the reality: when prices rise 6–8% a year, and your income doesn’t keep pace, every percentage point of savings matters. Cashback gives you a quiet, consistent way to recover some of that lost purchasing power — without sacrificing the things you buy.

This is especially true for high-frequency purchases. If you’re buying groceries, paying utility bills, filling fuel, or purchasing gifts regularly, cashback on each of those transactions adds up quickly. Over a year, it can amount to thousands of dollars that would otherwise have been spent.

Why is Cashback Important for Buyers?

Cashback isn’t just a marketing trick. There are genuine, practical reasons it matters for everyday buyers like you.

- It Reduces Your Real Cost of Living

Every cashback you earn effectively lowers the true price you paid for something. A $500 purchase with 5% cashback actually costs you $475. Do that across dozens of monthly transactions, and the savings become significant.

This is what makes cashback so powerful for everyday buyers. It doesn’t ask you to buy less or buy cheaper. It just makes what you already buy cost a little less — consistently, every month.

- It’s Passive — You Don’t Have to Work for It

Unlike discounts that require timing, coupon codes that expire, or sales that demand you wait, cashback is passive. Once you’re enrolled in a program, the rewards happen automatically every time you make a qualifying purchase.

This removes the cognitive load of ‘deal hunting.’ You shop when you need to, and the system takes care of rewarding you. For busy consumers — which is most of us — this frictionless approach to saving is invaluable.

- It Works Across Categories

Cashback isn’t limited to one type of purchase. Depending on the platform or card you use, you can earn rewards on groceries, dining, travel, online shopping, bill payments, entertainment — and yes, gift cards too.

This cross-category flexibility means cashback fits seamlessly into how people actually live and spend, rather than forcing them to change their habits to chase a reward.

- It Fights Inflation Silently

When prices rise, your money buys less. Cashback is one of the few tools that pushes back against this — not by lowering prices artificially, but by returning a portion of what you spend to your own pocket.

A consumer earning 4% cashback on $1000 of monthly spending gets back $480 over a year. That’s a meaningful buffer against rising costs, created entirely through spending that was already going to happen.

- It Encourages Smarter Spending Habits

When consumers become aware of cashback opportunities, they naturally start thinking more carefully about where and how they spend. They compare platforms, they plan purchases, they look for better rates. This mindfulness — even if small — leads to better overall financial habits.

Cashback is not just a reward mechanism. It’s also a gentle nudge toward financial awareness.

- It Builds Real, Long-Term Savings

One cashback reward feels small. Twelve months of cashback rewards across multiple categories feels like a bonus. Three years of consistent cashback earning can fund a holiday, an appliance, or a financial emergency buffer.

The magic of cashback is compounding consistency. You don’t need to change anything dramatically. You just need to earn it regularly and let it add up.

“Cashback is the smartest way for everyday buyers to save without sacrificing what they love. It works invisibly, consistently, and without effort.”

How Can Consumers Earn Cashback?

There are several channels through which everyday buyers can start earning cashback. Here’s an honest breakdown:

| Channel | How It Works | Best For |

|---|---|---|

| Cashback Credit Cards | Earn % back on every swipe; credited to card statement | High-frequency card users |

| E-commerce Platforms | Platform credits or wallet money on eligible orders | Online shoppers |

| Banking / UPI Apps | Cashback on bill payments, transfers, recharges | Digital payment users |

| Gift Card Platforms | Earn % cashback when purchasing gift cards for brands | Gift buyers & brand loyalists |

| Loyalty Programmes | Points per purchase, redeemable as cash or rewards | Brand-specific buyers |

Each of these channels has its own advantages. The smartest buyers often use a combination — earning cashback through their card, their shopping app, and their gift card platform simultaneously.

Gift Card Platforms: An Underused Way to Earn Cashback

Most consumers think of gift cards as a gifting tool — something you buy for someone else’s birthday or a festival. But forward-thinking buyers have discovered that gift card platforms can also be a powerful cashback vehicle for themselves.

Here’s how it works: when you buy a gift card for a brand you regularly use — say, a supermarket, a streaming service, or a clothing retailer — and that purchase comes with a cashback reward, you’ve essentially gotten a discount on money you were already planning to spend. You top up your favourite brand’s gift card, earn cashback on the purchase, and then use the card as normal.

|

🎁 Buying a gift card for a brand you love isn’t just gifting — it’s pre-loading your spending with a cashback reward baked in. It’s one of the simplest money hacks most consumers overlook. |

|---|

This is where platforms like PlusGiftCard come in. PlusGiftCard is a digital gift card platform built around the idea that buying and gifting should come with real rewards. When you purchase gift cards through PlusGiftCard, you earn cashback on your transactions — turning routine gift buying into a savings opportunity.

Beyond just cashback, PlusGiftCard offers gift cards across a wide range of brands and categories, giving buyers the flexibility to earn rewards on things they genuinely care about — whether that’s dining, fashion, entertainment, or everyday essentials. The redemption process is simple, transparent, and designed for buyers who want value without complexity.

For consumers looking to stretch their money further in a time of rising prices, gift card platforms with cashback programs represent one of the smartest and most overlooked tools available.

How to Maximise Your Cashback Earnings

Earning cashback is easy. Earning the most cashback takes just a little intention. Here are practical tips for buyers:

- Know where you spend most — focus cashback efforts on your highest-spending categories

- Use a cashback credit card for all large purchases and pay it off monthly

- Buy gift cards for brands you already shop at — earn cashback on pre-planned spending

- Check for seasonal cashback boosts — rates often increase during festival seasons and sales

- Don’t let cashback expire — redeem consistently rather than letting it accumulate and lapse

- Stack rewards where possible — some platforms allow cashback on top of existing discounts

The buyers who benefit most from cashback are not necessarily the ones who spend the most — they’re the ones who are most deliberate about where they direct their spending.

Common Myths About Cashback

Myth 1: “The cashback amounts are too small to matter.”

Truth: Even 2–3% cashback on $1000 monthly spending returns $20–30 per month, or $240–260 per year. That’s not small — that’s a meaningful financial cushion built automatically.

Myth 2: “Cashback programs are complicated.”

Truth: Most modern cashback platforms — especially gift card platforms — are built for simplicity. You shop, you earn, you redeem. The complexity people fear rarely exists in practice.

Myth 3: “Cashback makes you spend more than you should.”

Truth: Cashback rewards work best when applied on spending you were already planning to do. Used intentionally, cashback saves you money — it doesn’t encourage unnecessary spending. The key is discipline: earn cashback on needs first, wants second.

The Bottom Line: Cashback Is a Consumer’s Best Friend Right Now

In an economy where prices are rising and budgets are tightening, cashback is one of the few tools that consistently works in the buyer’s favour. It doesn’t require a lifestyle change. It doesn’t demand sacrifice. It simply rewards you for spending you were already going to do.

Whether you earn cashback through your credit card, your shopping apps, or a gift card platform like PlusGiftCard, the principle is the same: every rupee you spend is an opportunity to get a little bit back. Over time, those little bits become real savings — money that stays in your pocket instead of disappearing into the rising cost of living.

Start small. Be consistent. And let cashback do what it does best: quietly, reliably make your money go further.

Ready to earn Cashback on every gift card purchase? Explore PlusGiftCard – where gifting meets rewards.